As a business owner one is always looking for ways to maintain a constant stream of revenue. If you are selling a product or service, the sales are not always going to be consistent (unless you are Walmart, Amazon, Google, etc.). If you have employees and your payroll is due every two weeks, and sales have not been that great in the past two weeks, you still need a way to pay your employees. Perhaps it is far simpler. You own a business and next month is Christmas. You need $5,000.00 today so that you can buy the items that you are going to sell in December that are going to make your business $25,000.00. The problem is that you only have $2,000.00 cash in your business bank account.

This is where credit becomes crucial for a business. If you are one of those businesspeople who is looking for another option to finance your business, then this is the article for you. I am going to walk you through a bank that I found that has a very simple business credit card that you can get approved for with very little in the way of documentation. You heard me: no P&Ls, taxes, bank statements, or weeks of underwriting.

Best of all I have gone through this process personally. This is not some article that is going to provide you with hypothetical processes. I am going to explain my experience with this bank step by step.

Disclaimer – this is not a guarantee that you will get approved for this business credit card. I am not going to tell you that no matter how low your personal credit score is that there is some secret way of getting approved. This is not information for an individual who plans on getting this business credit card, running it up to the limit, and then disappearing. And YES, you are going to have to PG this credit card. If your business credit was good enough to get a loan without a PG, you wouldn’t be reading this blog post.

The bank that we are discussing today is Citizens Bank. Before we begin, you are going to need the following to increase your chances of getting approved:

- A business preferably greater than 2 years old

- EIN for business and SSN for sole proprietor

- Business address and phone number

- Equifax score of >680

- Website (optional)

While you can apply for business credit with a business that is less than two years old, your chances of getting an approval greatly increase when your business is greater than two years old. This is when you need to ask yourself, “When did I start this business?” Today is September 30, 2021. You might have incorporated last month but have been doing this business for the last five years. This is a small distinction, but one that you should keep in mind as you will have to answer this question about how long you have been in business.

If you are a business that is a corporation, partnership, or an LLC you will need an EIN. This number is like social security number for your business. You can obtain this number for free from the IRS, but if you have an attorney who is setting up your business for you, the EIN will be part of the process. Make sure that you have your documentation from the IRS that has you EIN.

You will need a business address and phone number. Obviously in today’s market working from home is normal so don’t have any hesitation about using your home address. There is a lot of data out there that will tell you that you need to get a virtual address if you do not have a business address other than your personal address. That was not my experience with Citizens Bank. Also, you need a business phone number that announces your business. This can be a cell phone, but it needs to be dedicated to your business. I have had a Google Voice number that I use for my business for several years. The great thing about using a Google Voice number is that you can select your area code and it is free. You can forward the Google Voice number to up to three phone numbers if you need to do so.

One of the best things about this business credit card is that the bank performs a soft pull of your Equifax credit report. What is a soft pull? When lenders pull your credit, they can perform a hard or a soft pull. A hard pull shows up on your credit report as an inquiry and remains on your credit report for two years. Anyone who pulls your credit will see the inquiry from the bank that conducted a hard pull of your credit. A soft pull does not show up on your credit report. This is very powerful. Citizens Bank is conducting a soft pull, and it from only one of your credit reports: Equifax.

If you are one of those people whose Equifax credit score is good, and Experian and Trans Union are not, then this is excellent news! Conversely, if you are one of those individuals whose Equifax score is one of your lower scores, then not so much. In an event it is responsible to check all three of your credit reports and know what range your scores are. If you do not have any idea, go over to Credit Karma, and get a look at your Trans Union and Equifax scores for free. These scores will not be the scores that are used by Citizens Bank, but you will have a good idea of where you stand and what you need to work on, if anything.

Finally, having a website will add legitimacy to your business profile. It is not mandatory, but it is a good idea to have one. If you need to establish a website, there are many options from WIX to WordPress. Now that we have all of that out of the way, let me walk you through my experience with Citizens Bank and the application for their business credit card.

On Thursday, September 16, 2021, I applied for the business credit card on Citizens Bank’s website. The application was straight forward. You will have to enter information about your business and your personal information. The application took about ten minutes. At 4:54 PM CST I immediately received the following email:

This email was the confirmation that my application was received. At 5:01 PM (seven minutes later) I received the second email:

This email directed me to go to their portal where I was asked to upload my ID along with my website information, both of which I provided.

On Friday, September 17, 2021, at 1:20 PM I received the third email:

This email directed me to call a toll-free number for a short interview. During this interview I provided information about my business: who I am, what I do, and how long I have been in business. I also provided my website again. The interview was no more than five to seven minutes.

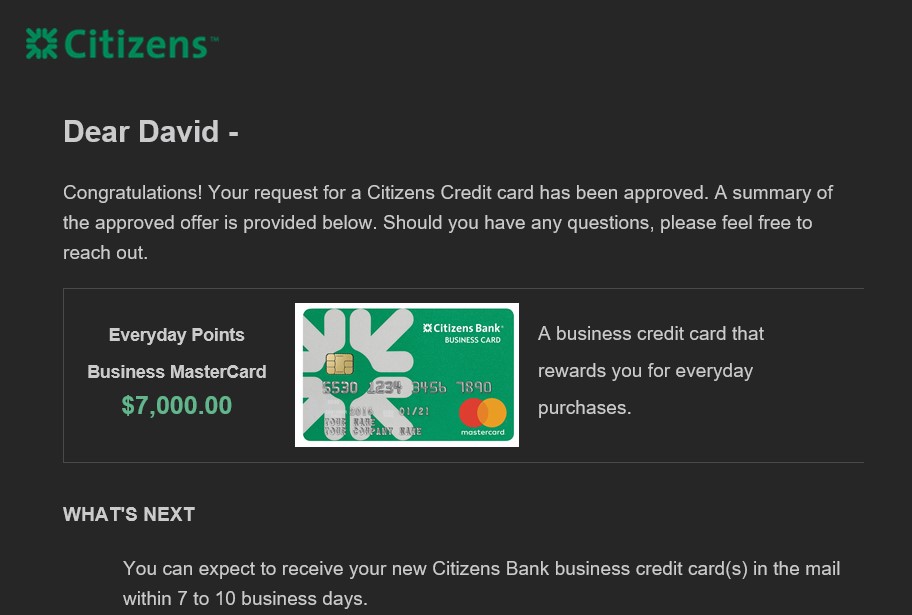

Finally, on the same day Friday, September 17 at 4:18 PM I received the following email:

You read that correctly. From application to approval was less than 24 hours. And finally on Thursday, September 30 (thirteen days later) I received my Citizens Bank business credit card.

I want to provide a few more data points about me and my business:

- My business is 4 years old

- My business is an S-Corp

- I used my home address and I use Google Voice for my business phone number (not listed with 411)

- I have a 700+ Equifax score

- I have a website

- I do not have any accounts with Citizens Bank

I had a very positive experience with Citizens Bank, and I personally endorse them and their business credit card product. Are you starting a business? Do you have a business and require assistance with getting financing? Feel free to message me today.

reallyb like you and atiba together you guys make a great team

LikeLiked by 1 person

Thank you.

LikeLike